Is Buy and Hold a good strategy?

First of all, we would like to state that “Buy and Hold” is not a completely wrong strategy. Anyone who bought the index at 17.76 in 1929 and kept their holdings can, at the time of writing, enjoy a total return of just under 20,600%. The entire stock market is the way to invest in success. The average annual return is approximately 10%. A fantastic investment, but here we can already identify a major problem; most people do not invest over the age of 93.

Time horizon

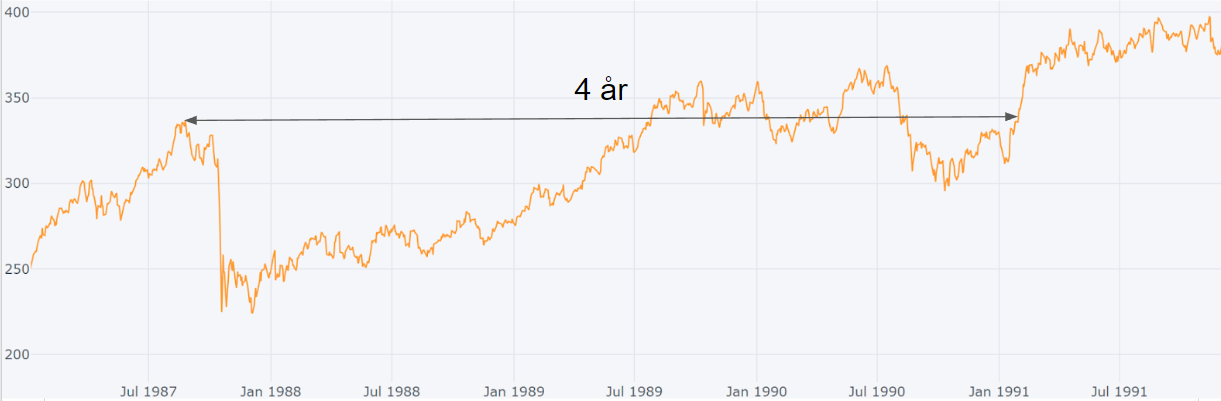

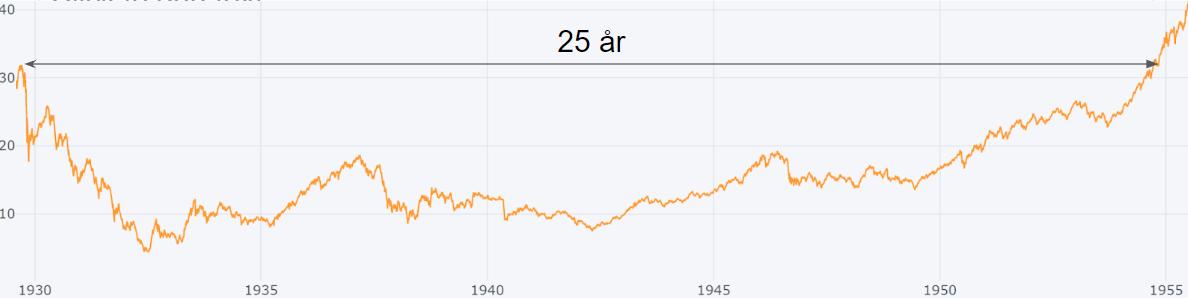

For buy and hold to work over time, you need to have just that, time. Below we see examples of time periods when the S&P 500 has not given a nominal return.

The “IT Bubble” and the “Financial Crisis”

“Black Monday”

“The Oil Crisis”

“Kennedy Slide”

“The Great Depression”

So you have to be able to keep the index very long to ensure a return which is not negative.

To achieve the average return of 10% per year, a time horizon is required that is likely to be longer than one's own life.

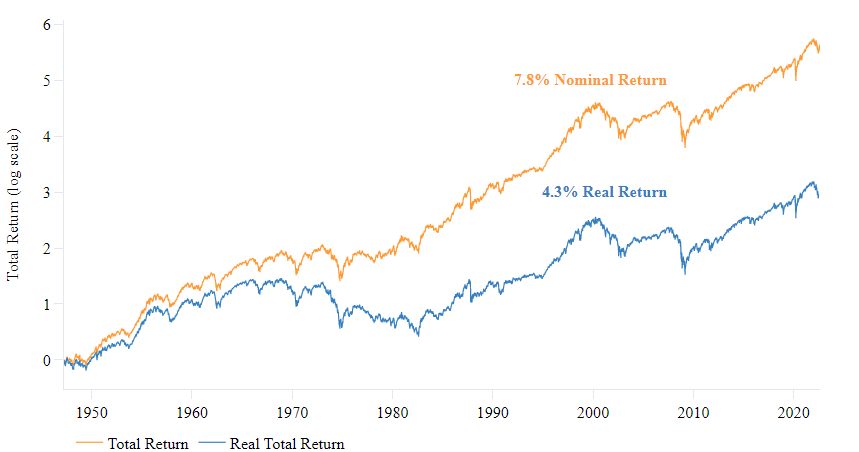

Then we have not taken inflation into account. Below we study an example of annualized nominal vs. real return.

Here too, we see that buy and hold over 70 years is not sufficient to achieve a nominal return of 10% per year.

For many, this strategy is not enough. Many of us want and need to generate alpha to achieve our savings goals. Most often, it is about saving up to a certain amount in a certain time.

Is it important to achieve a nominal return of 10% per year?

Not necessarily. You can certainly settle for a worse capital development, especially if you have time on your side. In any case, you who are reading this article probably have higher ambitions. You certainly want a financial security that an index cannot deliver.

How can ordinary people think to achieve security?

Timing is everything – have a structured process

We are often told that it is impossible to time the financial markets. To some extent, that is true. We cannot time exact bottoms and tops.

Either way, we can give ourselves the best chance of being successful in our trading. Increase the likelihood of success by being right in the longer cycles.

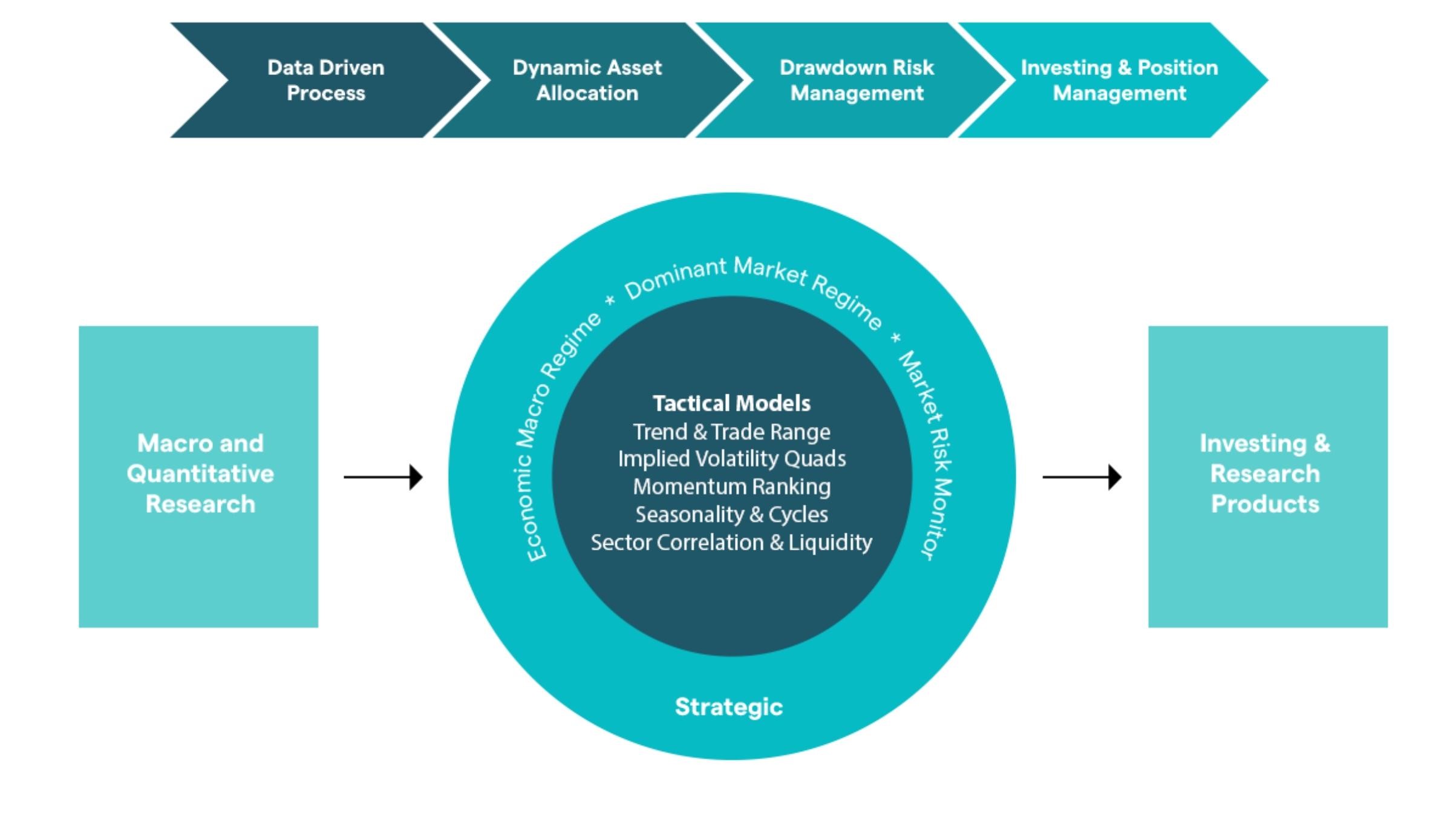

NeuroQuant uses a structured process that allows us to:

- Avoid major downturns.

- Know when to accelerate or brake.

- Protect capital

They do this through market analysis. I have long listened to Marknadspulsen with Erik Hansén where he shares different models depending on the time perspective. These models are put in context with each other and allow customers to get a good risk-adjusted return. It's everything from market regimes, broad indicators, seasonal patterns, flows, allocation, sentiment, proprietary data series and more.

Those of you who have been following along in 2022 have probably, like me, avoided the major downturn that has taken place.

Larger declines are problematic

Major downturns, like the ones we've seen in 2022, are problematic. They're psychologically taxing. It hurts to see your portfolio lose 30% of its value in a short period of time. Many people tend to sell when it hurts too much.

The result is permanent capital destruction.

It is also important to understand the recovery a portfolio requires to recover from a large loss. These recoveries are necessary to achieve an average return according to our savings goals.

Below we see the return of one dollar over 70 years in the S&P 500 compared to a “promised” return of 8% per year.

We can see that the 2007-2009 crash created a large gap between expected and realized annual returns. This gap has not been filled despite the historically strong bull market we have had from 2009-2021.

It becomes very clear why the gap remains over time when we study the table below.

| % Decline in Capital | % Return Required to “Break Even” |

| -5% | 5,3% |

| -10% | 11,1% |

| -15% | 17,6% |

| -20% | 25,0% |

| -25% | 33,3% |

| -30% | 42,9% |

| -35% | 53,8% |

| -40% | 66,7% |

| -45% | 81,8% |

| -50% | 100,0% |

| -55% | 122,2% |

| -60% | 150,0% |

| -65% | 185,7% |

| -70% | 233,3% |

| -75% | 300,0% |

The percentage increase required to break even in the event of larger losses is significantly greater than the percentage decrease.

If we avoid big declines, we don't need to risk capital on big rises. We don't need to be emotional and fall for FOMO in temporary bounces because we didn't lose money in the initial decline.

To what extent do we protect our capital, thanks to a clear, data-driven and repeatable process.

Valuation

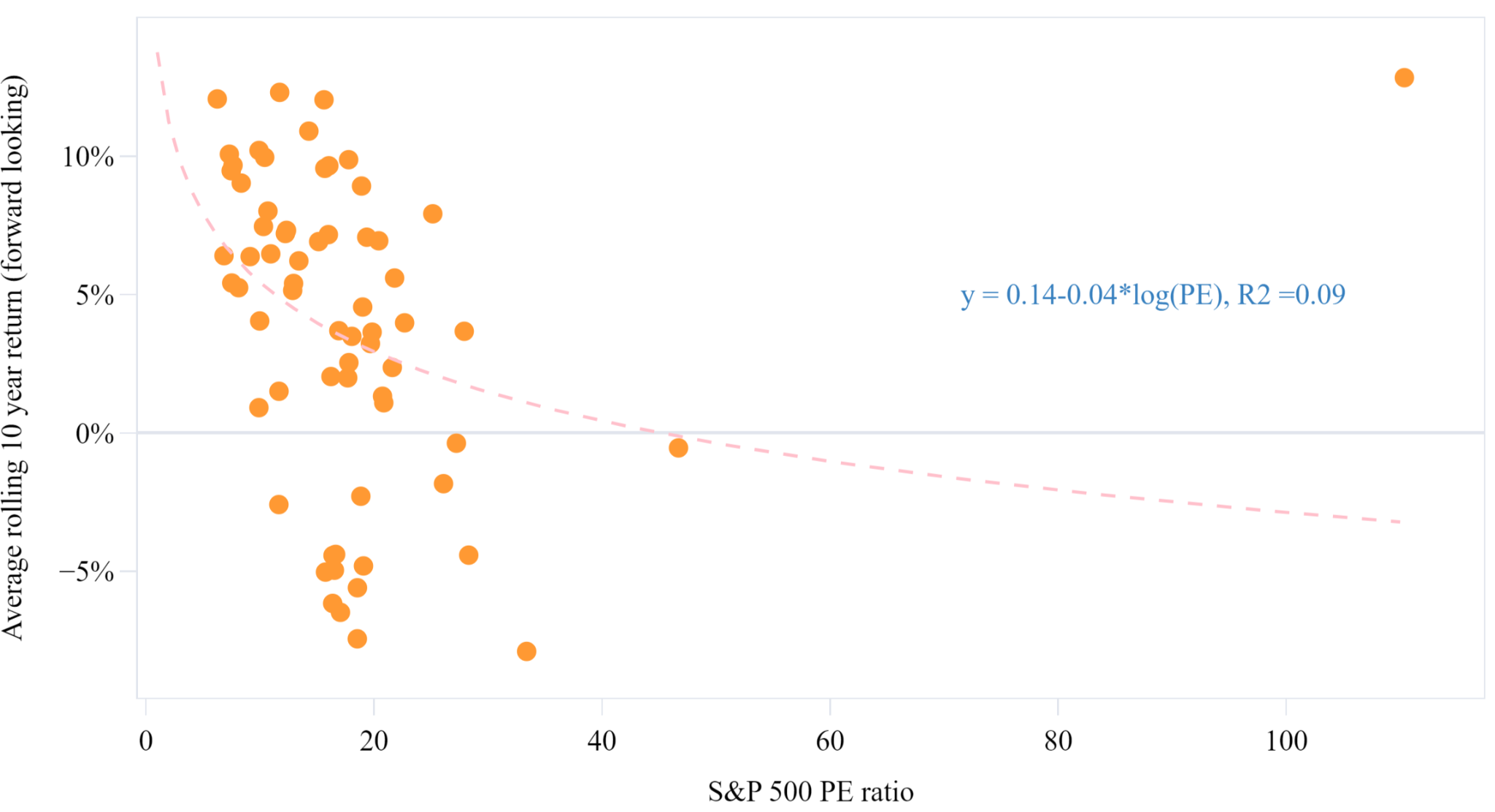

NeuroQuant has been clear that valuation is not a catalyst in the short-medium term (0-12 months). However, it is increasingly crucial in the long term (+3 years). Below we see a correlation between valuation and returns over the next ten years.

Generally speaking, we can say; the lower the valuation, the higher the expected return over the next 10 years.

According to this figure, there has only been one occasion (caused by large write-downs during the 2008-2009 financial crisis) when the S&P 500 has produced a positive return over the next 10 years when PE > 30.

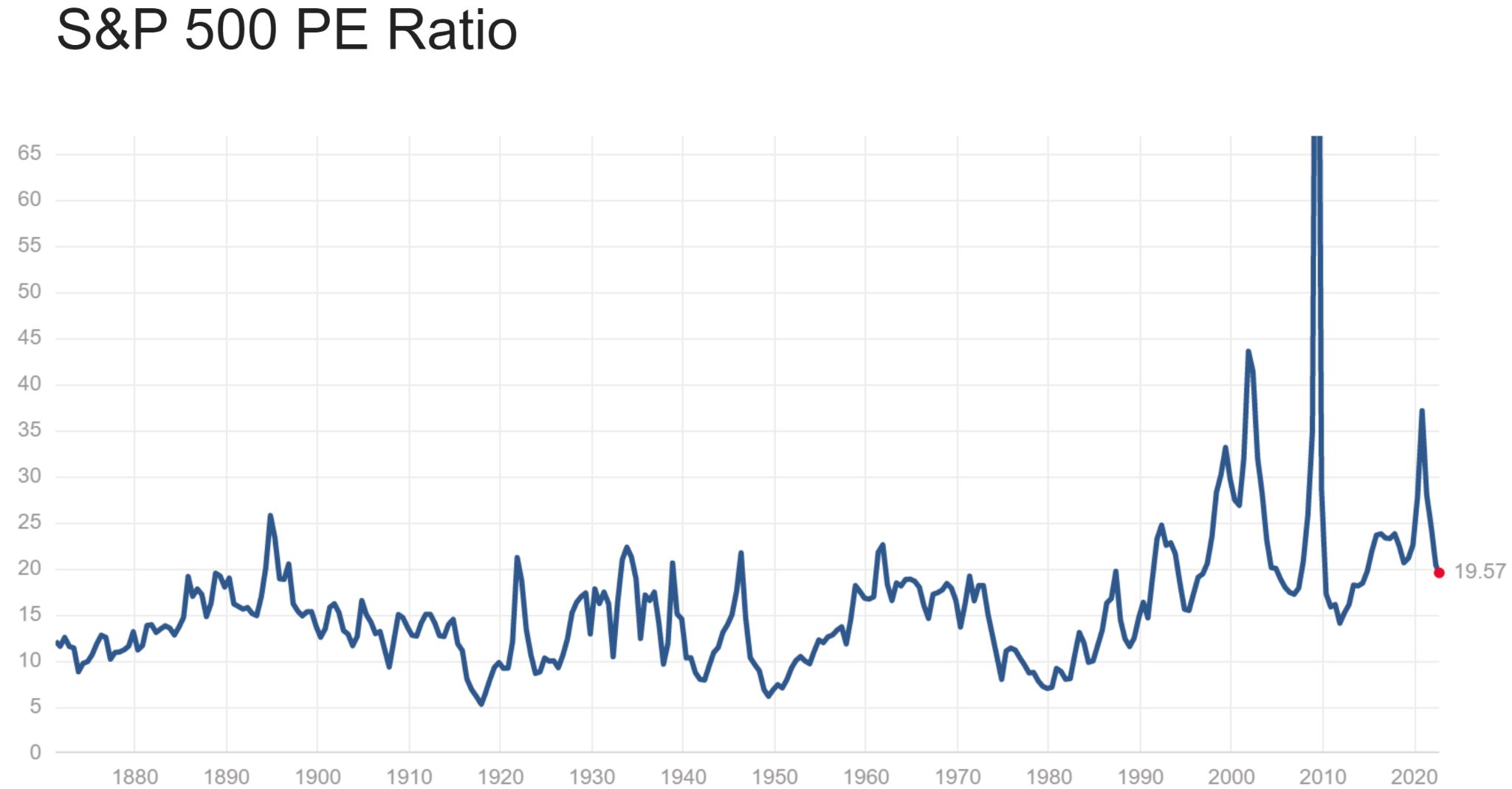

Below we see that PE ~ 35, in 2021.

When I listened to Erik Hansén in January 2022, he put valuation in context with, among other things, falling growth, rising inflation, tightening central banks, positioning, divergent risk appetite, trend shift in trend and trading range and decided to go underweight stocks. This has proven to be a successful decision.

“Show me the incentive and i will show you the outcome” – Charlie Munger

It is important to understand the incentives behind those who advocate a “buy and hold” strategy.

Those who produce financial products, ETFs and funds take a percentage of the invested capital. This means that they lose revenue if a player chooses to switch to cash.

Ask yourself the question “What are the incentives?” when you are being advised. The answer to this question offers nuance in decision-making.

In conclusion…

- Quantify the annual return you need to achieve your savings goals.

- Define your time horizon.

- Take inflation into account.

- Avoid major downturns at all costs.

- Take valuation into account in long-term savings.

If you can follow these five points, you will do well.

9 Comments

Ulf

3 year ago -Really well written

Linus Jacobsson

3 year ago -Thank you for your feedback Ulf!

Linus Jacobsson

3 year ago -Thank you for your feedback!

Thomas Berger

3 year ago -Many thanks Linus for a really good fact-based analysis with a concluding summary. I have long had the same opinion about why the proponents of “Buy n' Hold” recommend this strategy.

Linus Jacobsson

3 year ago -Thank you Thomas! It is very enjoyable to read those words. We have the opportunity to learn a lot on the platform that is NeuroQuant.

Jäger

3 year ago -You're heavy, Linus.

Linus Jacobsson

3 year ago -Thank you, will you??

Micke

3 year ago -Thanks for an interesting analysis!

I think if you bought Investor at the peak (June 2007) for 45 SEK and 10 years later it is worth 100 SEK (excluding reinvested dividends), then it should still be a good “buy and hold” investment over time, right?

How do you view reinvested dividends and monthly savings when thinking about "buy and hold" on a 10-year horizon?

Do you have analysis on that strategy?

Thank you for the answer 🙂

thank you

MRINVEST

Linus Jacobsson

3 year ago -Hey Mike!

Thanks for a good question.

There will always be cases where buy and hold worked out just fine! Likewise for the opposite. Let's play with the idea that you bought HM-b in 2007. Then you are back 50% today in absolute terms.

Let's take your Investor example. If you bought in 2007 at 45 and sold 10 years later, you had a development of 8.3% CAGR. Decent, absolutely! You can be satisfied there.

In that example, you should also be prepared to halve your money over 2 years.

If you had waited 2 years until the trend reversed and bought at SEK 30 and waited until 2017, you would have had a CAGR of 11.1%.

I haven't delved into the investor stock and what the fundamentals looked like in 2007, but the basic analysis remains the same;

Is the asset reasonably valued? Is the expected return in line with my savings goals?

Utilizing macro analysis and overweighting stocks when we have favorable conditions (revolution, expansion) is now a very sharp tool we can use via NQ.

Continuous monthly savings and reinvested dividends will absolutely provide returns in line with the market. As the article suggests, those returns will be mediocre. You also have to follow the strategy slavishly and buy when you have already lost 50% of your money. This assumes you are diversified enough and don't cut yourself into junk.

I prefer to buy assets (long term) when they are reasonably valued and I can forecast good growth in the coming years. Very little was reasonably valued in January 2021!

Hopefully my rambling has given you insight into my perspective!

Regards, Linus J