Adjust portfolio weights for volatility

Beginners like to focus on buying signals that should work according to technical analysis while professionals focus on diversification, portfolio weights and risk management!

We can have an edge and act on signals that work well over time, but without good position management we will still underperform the index or even lose all our capital.

During the years I have worked at brokerage firms, I have seen most of them fail despite having a lot of knowledge, interest and a working strategy.

After failure, you come back and try another strategy with new capital and the hope of success.

There are many different methods for managing positions. Googling Position Sizing will not help us.

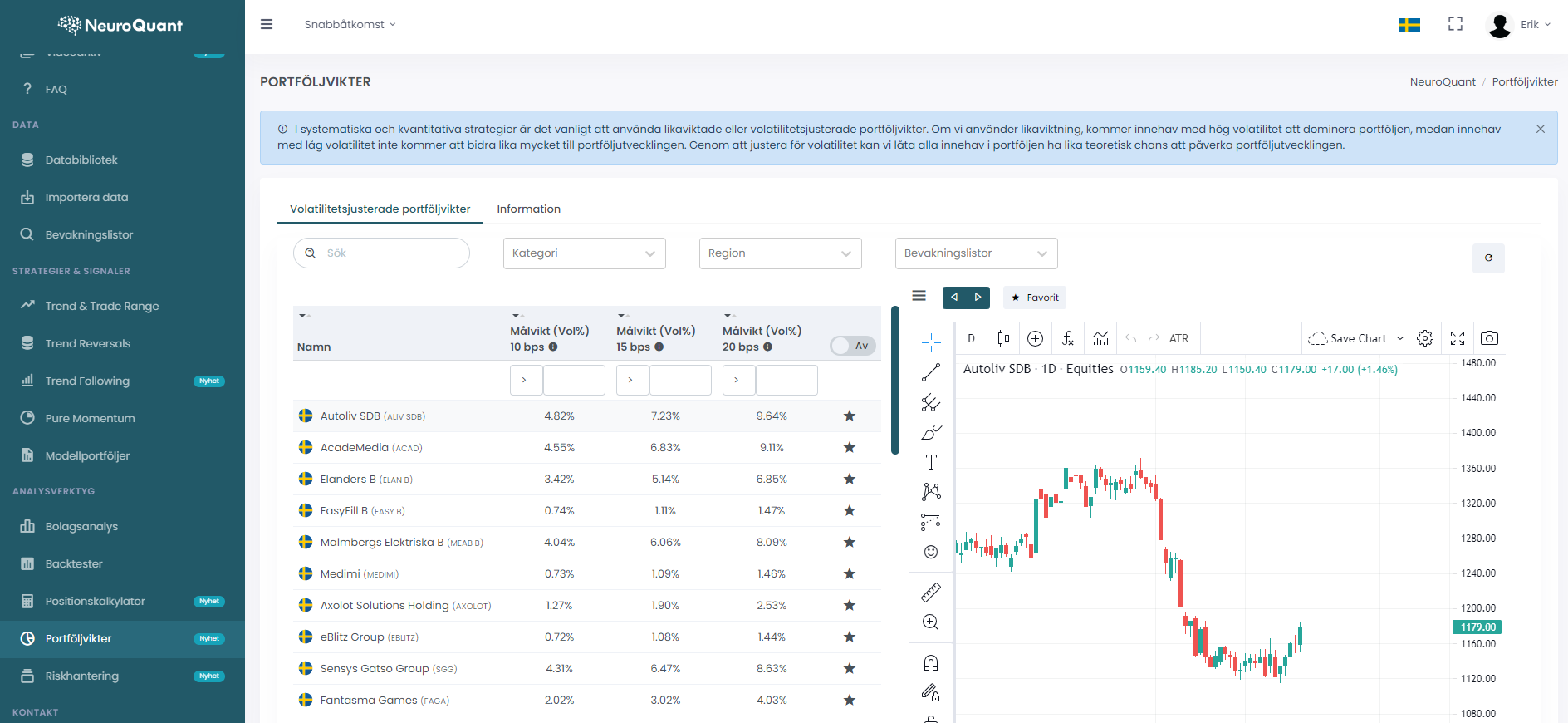

Volatility-adjusted portfolio weights

We use an algorithm that takes into account the volatility of the stock. It is a simple, yet powerful method that has worked well over time.

To calculate volatility, we use the Average True Range, which shows how much the stock moves during a "normal" day.

Stocks with lower volatility are given greater weight. Stocks with higher volatility are given lower weight. This is called Inverse Volatility, Risk Parity, Volatility Parity or Risk Parity Sizing.

We want all stocks in the portfolio to be involved and participate. Not that certain stocks dominate the portfolio and other stocks are “window dressing”.

Let's take an example.

- Stock A is trading in a low-volatility uptrend. The stock doesn't fluctuate much, but it is trending up.

- Stock B fluctuates a lot, both up and down. It may rank high on momentum, but the volatility is very high.

By adjusting for volatility, stock A will have a greater weight in the portfolio than stock B. In this way, we allow all holdings in the portfolio to have an equal theoretical chance of affecting the portfolio.

Weight all companies equally in the portfolio

Weight all companies equally in the portfolio

Many quantitative strategies equalize holdings. It's simple, which is a good thing. But personally, I don't think it's entirely logical.

Why would I want stocks that fluctuate a lot to dominate portfolio performance? I want to treat all holdings equally and let everyone contribute. I want holdings that trade in low-volatility uptrends to also affect portfolio performance proportionally.

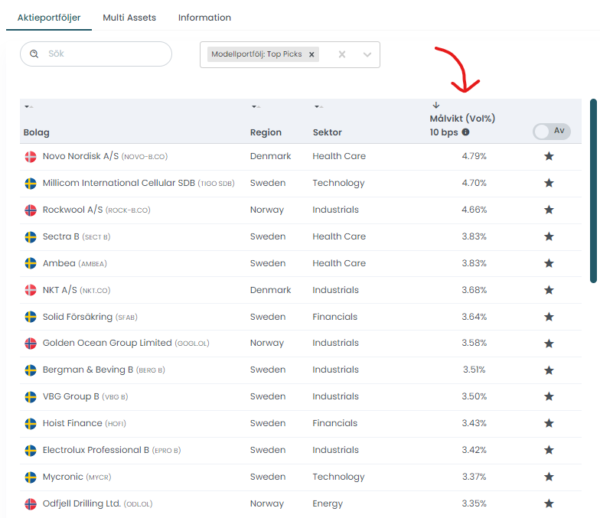

Our methodology for model portfolios

For our model portfolios, we adjust portfolio weights for volatility. The algorithm takes into account how much the stock moves during a “normal” day. We allocate 10 bps (0.10%) of volatility to each holding. Treats all companies equally.

Allocating 10 bps to each holding leads to a portfolio of approximately 30 stocks.

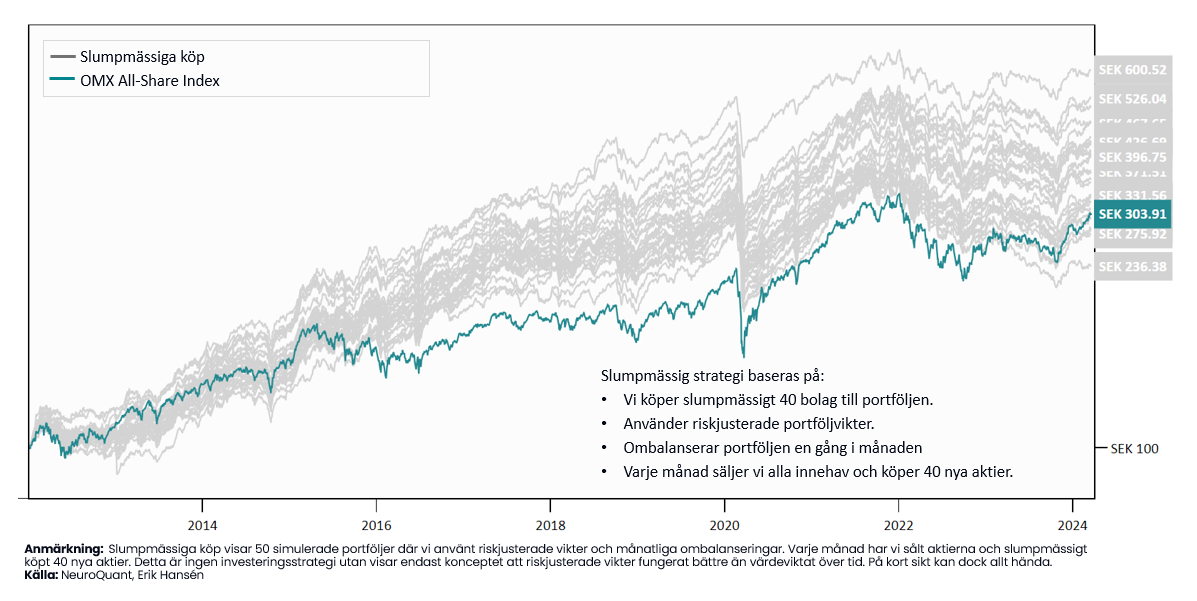

Random simulation with volatility-adjusted weights

With inspiration from the book Stocks on the Move, let's test how the method has worked historically.

- We randomly select 40 stocks to buy for the portfolio

- We adjust portfolio holdings for volatility

- Rebalances once a month

- Every month we sell all shares and randomly buy 40 new shares

The graph below shows 50 different simulated portfolios where we buy stocks randomly and adjust portfolio weights for volatility.

In the short term, anything can happen, but over time this method has worked better than value-weighted indices where the larger companies dominate the development.

In the short term, anything can happen, but over time this method has worked better than value-weighted indices where the larger companies dominate the development.

In the US, the S&P 500 has recently been fueled by the larger companies. We have also seen this before in history, but over time, volatility-adjusted performance has worked well.

If we trade a momentum strategy with volatility-adjusted portfolio weights, we will not choose stocks. They are the stocks that choose us. If it is larger companies that are winners, we will stay invested in these companies until they no longer show strong momentum.

Swing trading method

For example, we can trade oversold stocks in a positive trend according to the Trend & Trade Range model or breakouts from volatility contraction.

The strategies have an edge, but if we take too much risk, we can lose all our capital.

I saw many trading accounts blow up when I worked at a brokerage firm during Covid. Capital built up over a long period of time was quickly lost when people didn't take stops or reduce position sizes when volatility spiked.

"It's oversold! Now it's even more oversold. Oh no point in selling now. This is absolutely crazy. I'm just sitting here hoping for a turnaround."

Of course, this line of thinking combined with leverage doesn't work. We all understand that, but it's not as easy to be rational in the heat of the moment when you lack a method for position sizing, which leads to a loss of discipline.

“As a market participant, it is more important that you know that you always follow your rules than that you make money, because no matter how much money you make, you will inevitably lose it if you cannot follow your rules.

Mark Douglas

For swing trading, we use the position calculator in the platform. This calculator takes into account how much we risk in each individual trade if the price falls to the stop loss.

In model portfolios that are rebalanced once a month, no stop loss is used. We apply a different method of risk management. However, for swing trading, we recommend always using a stop loss.

In model portfolios that are rebalanced once a month, no stop loss is used. We apply a different method of risk management. However, for swing trading, we recommend always using a stop loss.

In the calculator we indicate how much of our capital we are willing to risk for each trade. This could be 1% for example. We also indicate how much volatility we are willing to tolerate, e.g. 0.5%. We can then also specify that the position must not be more than 5% of the portfolio value. This gives us 3 different position sizes where we take the smallest.

For swing trading, we can think of volatility as a factor we use to ensure we don't lose discipline. Increased volatility affects our brain. We don't want individual positions to cause us to lose the discipline to follow the strategy.

Access strategies and analysis

As a customer with us, you get access to an analysis platform with a wealth of educational materials, analysis, strategies, portfolios and other tools to increase your chances of successfully achieving your investment goals. As a premium customer, you have access to volatility-adjusted portfolio weights on all stocks we have in the database.

Open an account today or register one free demo account with delayed data and limited content.

Kind regards,

Erik Martin Hansen