Ray Dalio’s All-Weather Portfolio + Momentum

Ray Dalio popularized the concept of the “All-Weather Portfolio” through his hedge fund Bridgewater Associates, which is today the world’s largest hedge fund with over $100 billion in capital. Let’s try adding momentum to the strategy. But first, some background information on the concept of the all-weather portfolio.

Dalio wasn't necessarily the first to come up with the concept of a portfolio that could perform in all economic environments. The idea behind a diversified portfolio that is resilient regardless of economic circumstances has been around for a long time.

“You should have a strategic asset allocation mix that assumes that you don’t know what the future is going to hold”. – Ray Dalio

The inspiration for the All Weather concept likely comes from earlier economic theory and portfolio theory, particularly from Harry Markowitz's work on “Modern Portfolio Theory” in the 1950s, where the idea of spreading risk across different asset classes to maximize risk-adjusted returns began to gain traction.

However, Dalio took this further by developing a specific asset allocation that attempted to balance risks between different economic environments (growth, recession, inflation, deflation), which became the basis for the All Weather Portfolio. This strategy became highly influential and distinctive precisely through Dalio's detailed analysis and implementation of the idea.

The strategy is based on the idea that no one can predict the future with certainty, and that a portfolio must therefore be well diversified to handle different types of market conditions (e.g. growth, recession, inflation and deflation).

“I knew which shifts in the economic environment caused asset classes to move around, and I knew that those relationships had remained essentially the same for hundreds of years. There were only two big forces to worry about: growth and inflation. Each could be rising or falling, so I saw that by finding different investment strategies – each one of which could do well in a particular environment (rising growth with rising inflation, rising growth with falling inflation and so on.” – Ray Dalio

Holdings in All-Weather Portfolio

- 40% TLT (Long-term bonds)

- 15% IEI (Medium Term Bonds)

- 30% VTI (Global Equities)

- 7.5% GLD (Gold)

- 7.5% DBC (Raw Materials)

How has the strategy worked?

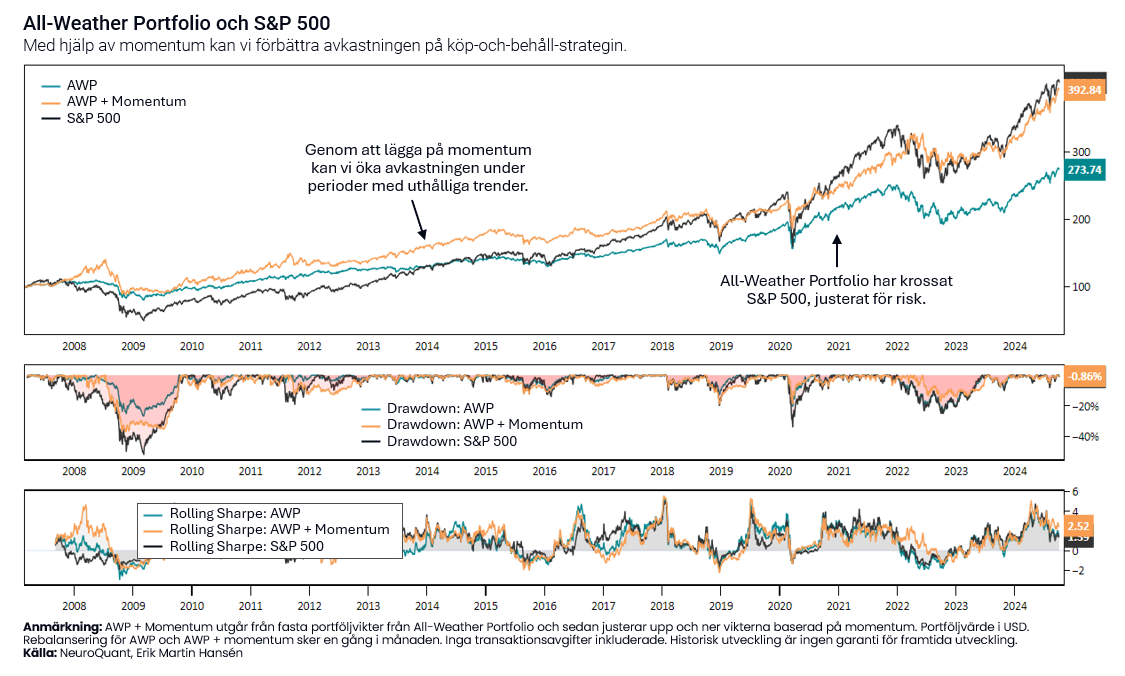

The All-Weather Portfolio has outperformed the S&P 500 in risk-adjusted terms, with strong performance at significantly lower volatility. See the strategy's performance in the graph below.

The high risk-adjusted return is partly due to the fact that the backtest includes a couple of bear markets where bonds have worked very well as diversifiers. It has also worked well because gold and commodities have contributed positively to the portfolio over various periods.

The S&P 500 has had a maximum decline of almost 60%, compared to about 30% for the All-Weather Portfolio. The emotional rollercoaster has therefore been less pronounced with this all-weather portfolio.

Can we improve the strategy?

Ray Dalio's All-Weather is a strategic buy-and-hold strategy with fixed holdings and weights. The portfolio should be rebalanced at least once a year to rebalance the risk distribution across assets.

Why not use momentum to weight up assets that are trending strongly and weight down those that are trending weaker?

For momentum, in this case I use our calculation that adjusts for volatility. The result is surprisingly good. No optimization has been done to fit historical data, as that would not help us moving forward. We aim for something robust that works even if history does not repeat itself.

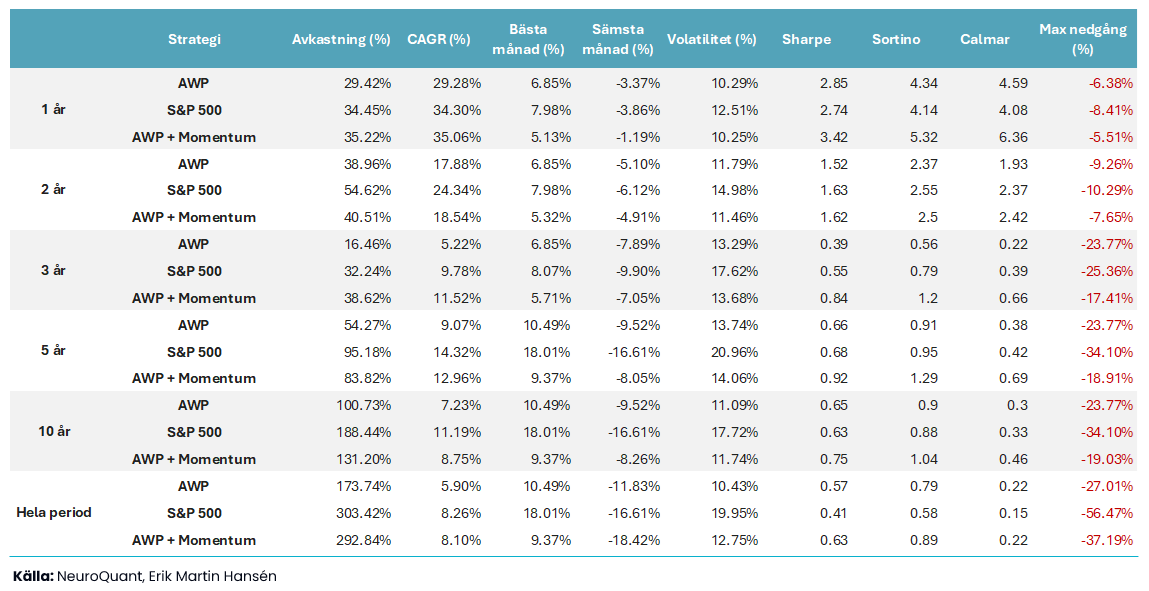

In the table below we can take a closer look at the statistics. Most people focus on total return or CAGR, but if we are evaluating a strategy it is important to also look at maximum drawdown and volatility. A strategy with high returns but also high volatility and deep drawdowns is easy to abandon at the wrong time, which can be very costly.

In the table below we can take a closer look at the statistics. Most people focus on total return or CAGR, but if we are evaluating a strategy it is important to also look at maximum drawdown and volatility. A strategy with high returns but also high volatility and deep drawdowns is easy to abandon at the wrong time, which can be very costly.

The next step is to test the method on a different universe of ETFs to see if the strategy is robust. If the strategy doesn’t work on a different universe, it’s likely not robust, and it may have been a coincidence that it worked on the ETFs we tested above. A rule of thumb is that a strategy that only works on a specific market is often overoptimized and likely won’t work in the future.

Summary: The best strategy is the one we can stick to over time. How would you handle a 60% decline in the stock market? Major declines happen a couple of times in most people's investing lifetimes. The last thing we want to do is sell out at the wrong time.