Why rebalancing is crucial in systematic strategies

On the platform, we offer portfolio weights adjusted for volatility to those of us trading systematic strategies. This is very unique. With the help of these, we can regularly rebalance portfolios, which is one of the most important aspects for success when following a systematic investment strategy, such as momentum.

Which stocks we buy is important, but how much we buy and sell is of course very important because it will affect the result. Most investors buy and hope for the best, but that is not a strategy.

What does rebalancing mean?

Rebalancing involves restoring the allocation of holdings to desired levels after a certain period of time. Rebalancing may sound time-consuming and tedious, but it has a profound effect on long-term returns and risk management.

Here are some of the reasons why rebalancing is crucial, especially when trading a strategy like momentum.

1. Stick to the rules of the strategy

Systematic strategies are built on clear and defined rules, and momentum is no exception. To ensure that the strategy follows its original rules, it is important to regularly reassess the portfolio and adjust it to maintain the right exposure to the assets that still show strong momentum.

2. Reduce risk by avoiding overexposure

When certain stocks perform well over a period of time, their value increases and takes up a larger portion of the portfolio. This can create an imbalance and overexposure to these stocks, which increases the portfolio's risk profile. If that stock suddenly turns down, it can mean large losses.

Rebalancing acts as an automatic risk control by selling off parts of the assets that have grown too much and reinvesting in other parts of the portfolio. In systematic strategies, such as momentum, this can be especially important because you are constantly chasing the latest trends. Restoring balance provides protection against sudden market movements and ensures that no single asset dominates too much.

3. Optimize returns by following market cycles

Momentum strategies are based on the idea that winners tend to stay winners for a while. But trends change, and a stock that performed well over the past six months may not do so next month.

By rebalancing, you can ensure that your portfolio is always comprised of the stocks currently showing the strongest momentum. This maximizes the potential for continued returns as the portfolio is regularly adjusted to reflect market dynamics.

If you do not rebalance, there is a risk that you will retain assets that no longer have the same strength, and thus miss opportunities for higher returns in other parts of the market.

4. Rebalancing and systematics go hand in hand

A systematic strategy is about removing subjective decisions and instead letting data-driven rules guide the composition of the portfolio. Rebalancing is a natural part of this process and should be considered an extension of the strategy itself. Without regular rebalancing, the strategy becomes inconsistent, and this increases the risk of the portfolio drifting away from its original goals and guidelines.

Having fixed rebalancing intervals, such as every month, makes it possible to stay disciplined and ensures that the portfolio constantly follows the parameters that your strategy requires.

A crucial component of all systematic strategies

Rebalancing is not just an administrative task; it is a critical component of any systematic investment strategy. When trading momentum or any other quantitative strategy, rebalancing ensures that we stick to the rules, reduces the risk of overexposure, and optimizes returns by continuously adapting the portfolio to market changes. By regularly readjusting the portfolio, the strategy becomes both more robust and more consistent over time.

How often should we rebalance?

How often you should rebalance a momentum strategy depends on several factors, including the type of momentum strategy you are using and the time horizon the strategy is designed for. Monthly rebalancing is often a good compromise between capturing momentum without incurring too frequent transaction costs.

If your rebalancing is very frequent or with small adjustments, transaction costs (brokerage and slippage) can start to eat into the profits from following momentum.

Here are two scenarios where it may be beneficial not to rebalance:

1) Transaction costs exceed expected benefits:

If your rebalancing is done very frequently or with small adjustments, transaction costs (such as brokerage and taxes) can start to eat into the gains from following momentum. A common approach is to only rebalance if the change in the portfolio is large enough to justify the costs, for example if a stock's weight has deviated more than 5-10% from your initial weighting.

2) Low volatility or stagnant market:

During periods of low market volatility, where stocks move marginally and changes in momentum are small, it may be beneficial to postpone rebalancing. If the market is stable and no major movements are occurring, there is little reason to make major changes. It may be better to wait until the market or stocks exhibit more significant price movements.

How do we know how much to buy or sell?

When it comes to deciding how much to buy or sell when rebalancing a portfolio, there are several approaches to consider. The most common options are equal-weighted portfolios and adjusting weights for volatility. Both approaches have their own advantages and disadvantages, and which one you choose depends on your investment philosophy and risk management.

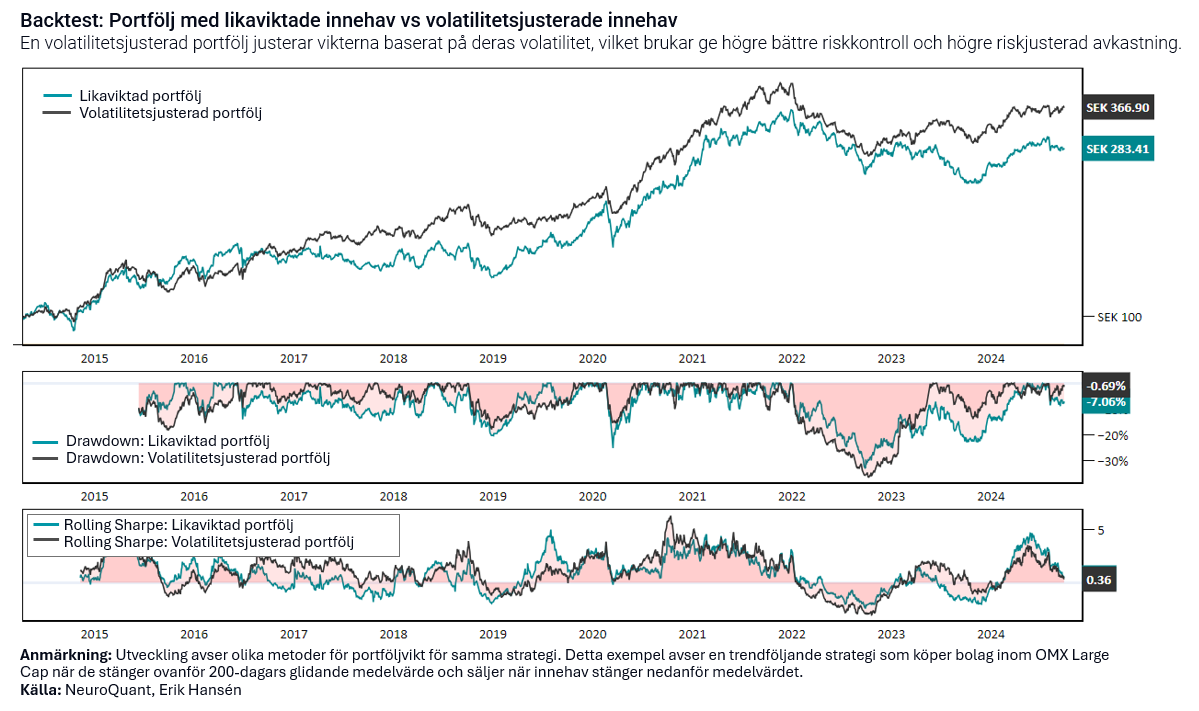

Let's look at the development of a strategy where I have chosen to use two different methods for weighting the holdings. The backtest refers to a simple trend-following strategy that buys stocks that close above their 200-day moving average and sells when the stocks close below the 200-day average. The investment universe consists of companies within the OMX Large Cap.

The results show that adjusting holdings according to their volatility has given a higher risk-adjusted performance. However, anything can happen in the short term where performance can often be random.

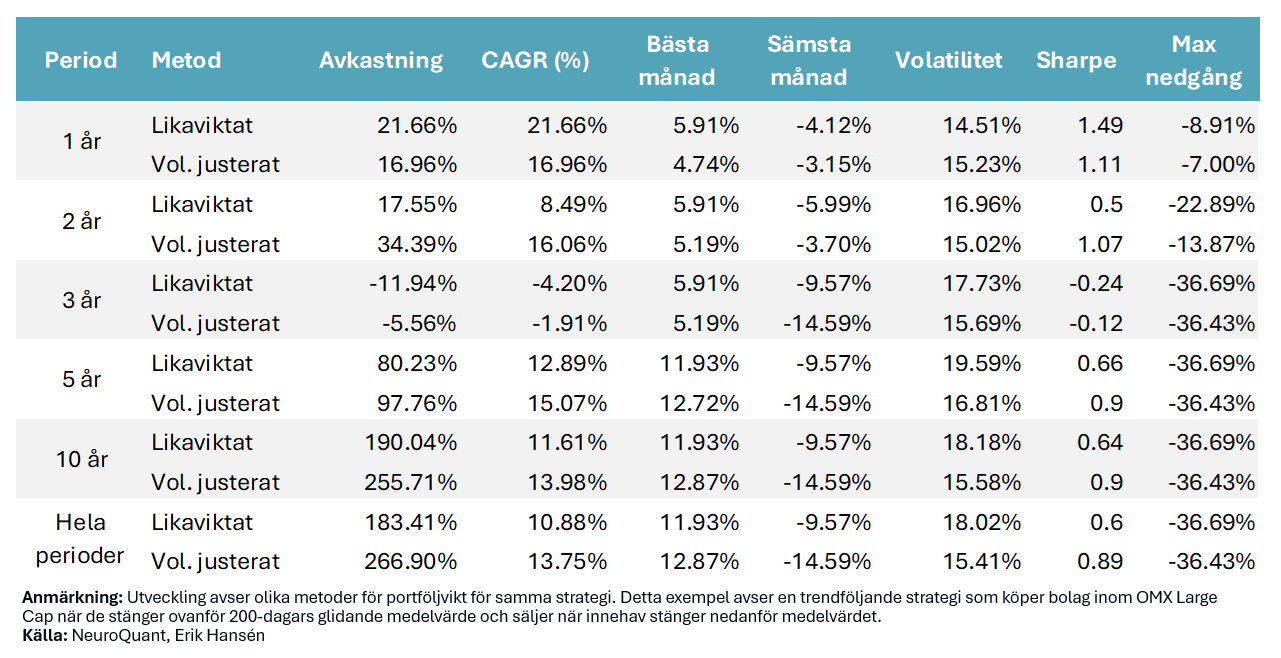

In the table below we see that the volatility-adjusted Sharpe is 0.9 compared to 0.6 for the portfolio where we have equally weighted the holdings. The volatility is also lower when we have adjusted the weight of the holdings in the portfolio according to their volatility.

In the table below we see that the volatility-adjusted Sharpe is 0.9 compared to 0.6 for the portfolio where we have equally weighted the holdings. The volatility is also lower when we have adjusted the weight of the holdings in the portfolio according to their volatility.

Let's take a closer look at the different methods:

Let's take a closer look at the different methods:

1. Equally weighted portfolio

An equally weighted portfolio means that you invest the same amount in each asset, regardless of its market value, volatility, or other characteristics. For example, if you have 20 stocks in your portfolio, you invest 5% of the portfolio's value in each stock.

Advantages of the equal weighted method:

Simplicity: This method is easy to implement and understand. You don't have to make complex calculations based on volatility or other factors.

Natural diversification: By equally weighting the portfolio, you avoid large stocks dominating the portfolio, which can provide better diversification compared to a market-weighted strategy where large companies are often overweighted.

Potentially higher returns: Historical studies show that equal-weighted portfolios often outperform market-weighted indexes over the long term, because you regularly sell stocks that have risen a lot and buy more of those that have fallen behind (which works well if stocks tend to oscillate).

Disadvantages of the equal weighting method:

No consideration of risk: Equally weighted portfolios do not take into account differences in volatility between stocks. Stocks with higher volatility can increase the overall risk in the portfolio.

2. Volatility-adjusted portfolio

In a volatility-adjusted portfolio, we adjust the weights of stocks based on their historical volatility. The idea is to assign less weight to more volatile stocks and more weight to stocks with lower volatility to reduce overall portfolio risk.

Advantages of the volatility-adjusted method:

Risk control: By adjusting weights according to volatility, you reduce the risk of a single, volatile stock dominating the portfolio's risk profile. This can make the portfolio more stable and less sensitive to sudden market movements.

Better risk-adjusted returns: By allocating more capital to more stable assets, you can potentially achieve better risk-adjusted returns. The portfolio becomes less sensitive to sharp declines, which can be especially useful in volatile markets.

Disadvantages of volatility-adjusted method:

More complexity: Calculating volatility weights requires more data and calculations than an equal-weighted strategy. You need to monitor volatility on an ongoing basis and adjust the weights with each rebalancing.

Following risk instead of return: By allocating less to more volatile stocks, you risk missing out on big profit opportunities in these stocks, as many of the most volatile stocks are also the ones that can provide higher returns over time.

Higher exposure to low-volatility stocks: You risk overexposing your portfolio to stocks with low volatility, which does not always mean low risk. Low volatility can also mean that a stock has limited growth potential. We avoid this by having a good method for stock selection.

3. Hybrid method (Equal weighting with volatility adjustment)

A third method for balancing simplicity and risk control is to first apply an equally weighted portfolio but then adjust the weights based on volatility. For example, you could start with an equally weighted allocation and then reduce the weight slightly for stocks with extremely high volatility.

Advantages of the hybrid method:

Balanced risk and simplicity: By combining equal weighting and volatility adjustment, you get both the simplicity of having an equally weighted portfolio and the reduced risk of adjusting for volatility.

Flexibility: This method allows you to have some control over how much risk you want to take, while still having the opportunity to capture the returns from more volatile stocks.

Disadvantages of the hybrid method:

Trade-offs: While this approach balances risk and return, it may result in you not fully utilizing the benefits of either approach. You may not get the full risk reduction that you would with a fully volatility-adjusted portfolio, and you may miss out on the opportunity for higher returns from the most volatile stocks.

Summary

Equally weighted portfolio is simple, naturally diversifying, and potentially more profitable in the long term, but it does not take risk into account and can increase portfolio volatility.

Volatility-adjusted portfolios reduce risk by reducing the weight of volatile assets, which can create a more stable return, but you risk missing out on large profit opportunities.

The hybrid approach can provide a good balance between risk and return by combining the simplicity of equal weighting with risk control from volatility adjustment.

Which method you choose should depend on your risk appetite and strategy. Personally, I prefer to adjust for volatility, as I like the idea of allocating more risk to stocks that are in low-volatility uptrends. These trends often tend to last longer than you expect.